Though payment declines are a fairly regular occurrence in online transactions, there are some types of declines that are more immediate than others. For example: False declines, which is when a legitimate purchase is wrongly declined by a bank or processor, add up to around $443 billion in lost revenue every year, according to a Aite-Novarica report that surveyed enterprise companies that take in $100 million and $999.9 million in annual revenue.

If you’re experiencing high decline rates, then you’re likely also experiencing low authorization rates. Lowering the former will increase the latter – and it’s important for merchants to strive for high authorization rates, as this is a strong indicator not only for their company’s financial performance, but also for the health of their brand among their customer base.

In this article, you will learn why authorization rates are a key metric for enterprise merchants and discover the common causes for high declines rates and low authorization rates. You will also receive strategies for increasing payment authorization rates.

Why authorization rates are critical for merchants

Whether you’re in eCommerce, retail, travel, gaming, delivery or the subscription business, enterprise merchants should be keeping a close eye on their payment authorization rates. This is a key metric that can shed light on how well your payment infrastructure is serving your financial and brand objectives. Consider payment authorization as a way to analyze the health of your transaction setup.

The payment authorization rate corresponds with revenue in that a high authorization rate means that there are more instances of payment success than there are payment failures. This means that more payments are being authorized successfully, and more successfully authorized payments will lead your business to increased profits.

Payment authorization rate can also be an indicator of the quality of your customer experience. A high authorization rate could indicate that payments are running smoothly without any friction and without any avoidable declines. Customers’ payments are going through and if you have low refund and chargeback rates, this could also mean that your customers are satisfied with the overall product and service of your brand.

Finally, a high authorization and low decline rate, coupled with a low chargeback rate, could mean that fraud or fraud attempts are low and that your payment fraud prevention measures are working.

Common causes for low authorization rates

Declines and payment failures can be grouped into two main categories: soft declines and hard declines. It’s important to understand the differences between these two categories and to also understand what each decline code means. Every bank and PSP has their own set of decline codes — Stripe has a comprehensive list of generic codes as well as their own codes — so familiarize yourself with your setup and dive deep into the reasons for declines in your business. You can also cross-reference them with the Payrails list of result codes.

Soft declines

Soft declines happen when an issuing bank doesn’t authorize a payment because of technical issues, suspected fraud or issues on the cardholder’s end. Soft declines are temporary failed authorizations and can be resolved quickly by addressing the reason for the decline. About 80-90% of declines are soft declines.

One common reason for soft decline is that there are insufficient funds available for the transaction – this is the case for 44% of soft declines. Some issuers aren’t so specific in their decline reasons, so insufficient funds might also just show up as “do not honor”. “Do not honor” also shows up if a payment has failed repeatedly – in fact, it’s the most common error message as a lot of issuers group many different things into this status.

Another common reason for soft declines is if the payment processor, issuer or any other technical layer in the transaction process is unavailable. This might be due to routing errors or technical downtimes. The good news is that merchants are able to solve for soft declines by implementing a series of fallback solutions into their payment infrastructure. More on that below.

Hard declines

Hard declines, on the other hand, are not as easy to solve for the merchant and are often permanent. One major reason for hard declines is outdated or inaccurate card information. This accounts for 1 out 5 of hard declines. The other major reason is if fraudulent activity has been detected, if the card has been reported lost or stolen or if the card has been flagged in the past for suspected fraud.

Though hard declines are more difficult to manage once they occur, merchants can implement prevention measures so that fewer hard declines, especially fewer false declines, occur.

How to solve declines and increase payment authorization rates

Dive into your transaction data and understand the reasons for your low payment authorization rate. Are your declines mostly due to cardholder issues or technical availability? Do you have a high fraud rate? Once you understand the reason or reasons for your business’s network declines, you can start implementing solutions that will reduce payment failures and will help you to achieve a high payment authorization rate.

How to solve for insufficient funds

Insufficient funds is the most common reason for soft declines, but it’s also one of the easiest to solve. By implementing a couple of key features into their checkout page, merchants can reverse or prevent insufficient fund declines and as a result increase the number of payment authorizations.

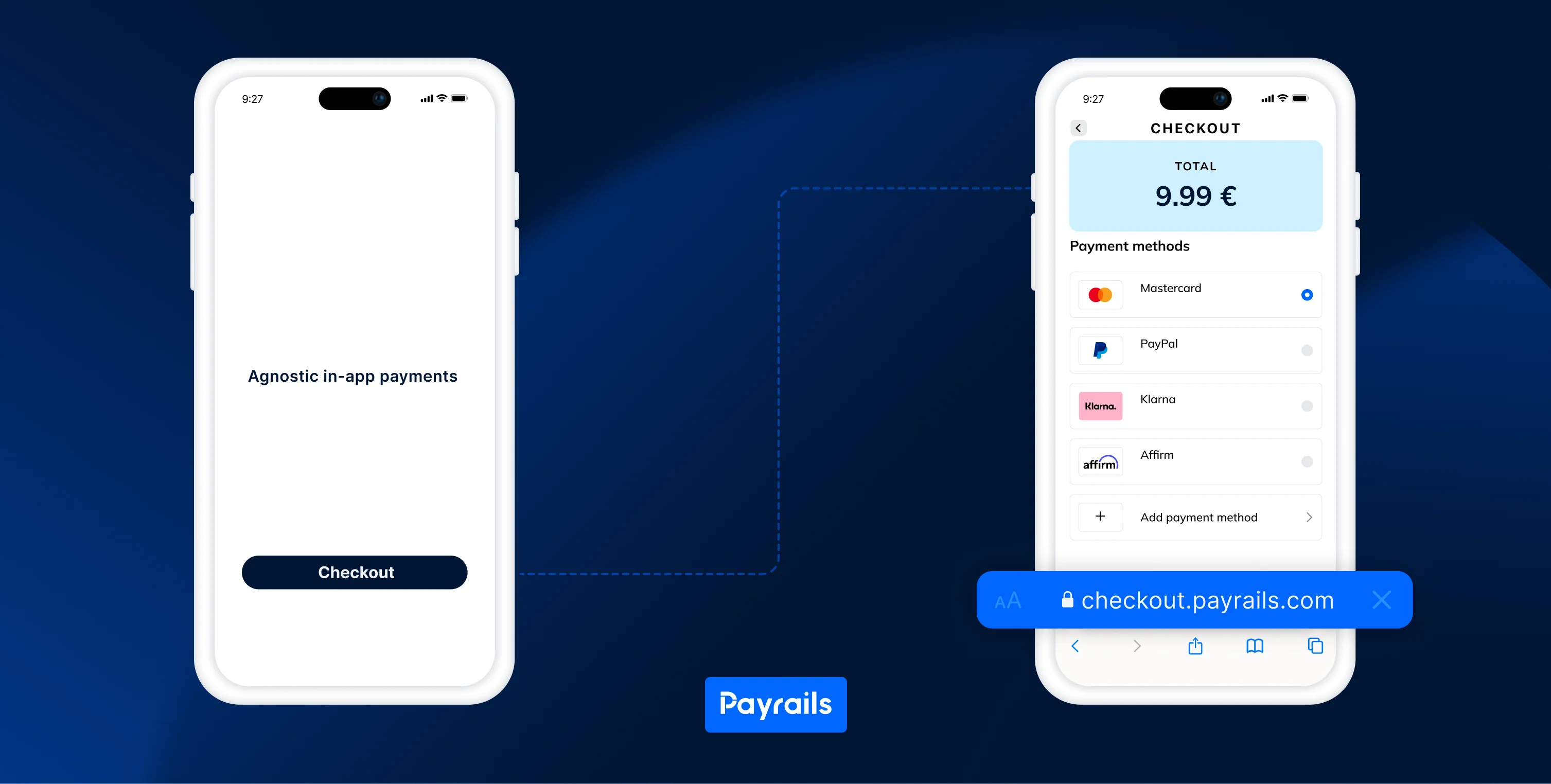

1. Add alternative payment methods (APM)

It’s a smart idea for merchants to offer alternative payment methods to their checkout page in case one payment method doesn’t have enough funds tied to it. Or perhaps the funds are insufficient but the payment method that is being used is turning up a false error. Either way, having multiple different payment method options available will increase the likelihood of a successfully authorized transaction. It will also add to the customer experience, as customers prefer to use the payment method that they are familiar with or that is commonly used in their country or region.

To save time, money and resources, merchants might want to consider integrating a payment operating platform or payment orchestration layer, which lets them connect to multiple payment methods, including local APMs, without having to integrate them all one-by-one, by themselves.

2. Offer buy now, pay later (BNPL)

Another way of tackling an insufficient funds decline and to improve payment authorization is to offer a buy now, pay later payment option. BNPL market is expected to reach a valuation of nearly $600 billion by 2026. Big players in this space are Klarna and Afterpay, and more established payment methods like PayPal have also been adding a BNPL feature into their product.

BNPL functions like a credit system in that the customer can choose to pay the transaction amount in 14 or 30 days, or pay off the amount in installments, which usually incurs some interest. A Similarweb survey has found that customers prefer BNPL for its convenience, with nearly 32% of respondents saying that BNPL was their only option as they didn’t have the finances to cover the purchase at the time.

3. Change billing date

This one is especially relevant for subscription businesses: Insufficient funds occur most often at the end of the month, before the next paycheck cycle. In order to avoid an insufficient funds error, move the date when you usually charge the recurring payment to the beginning or middle of the month when your customer is more likely to have the funds needed to cover the payment.

How to solve for processor unavailability

If you’re an enterprise merchant and you’re only using one processor, then you’re setting yourself up for failure: if your processor goes down or experiences technical issues during the payment authorization stage, then the payment will be declined. Processor unavailability can be a headache, especially since it can lead to false declines that could have been avoided. But there are a few ways to solve this problem.

1. Payment routing

As a merchant, it’s best practice to have at least four or more PSPs integrated into your system. Not only does this help you to get the best processing rates, it’s also a failsafe in case one of the processors becomes unavailable during transaction authorization. If you have multiple PSPs, you will be able to implement dynamic payment routing. This feature allows you to set up routing rules that if one processor is unavailable, the payment is automatically re-routed to a different integrated processor.

2. Automatic retry

Occasionally a technical decline is just a temporary hiccup that can be resolved instantaneously by trying the payment again. However it’s a hassle for customers to have to retry the payment manually. This involuntary churn accounts for 34% of the overall churn rate. To solve this, merchants can implement an automatic retry feature that recovers failed payments without the need for customer intervention. With a retry engine, merchants can configure how long to wait before trying the payment again and the maximum number of attempts before sending the payment to a different processor or prompting for a different payment method.

How to solve for outdated payment information

Sometimes card information is missing or expired, or a customer’s card has been recently renewed and the information that was stored in your system is no longer accurate. Inaccurate payment information is a common reason for card declines that can be combated with the following strategies.

1. Collect billing information

For first-time customers, be sure to collect as much billing information as possible to avoid declines in the future. Full billing details include the billing address, name on card, card number and the card expiration date. Having all of this information will make it easier for the issuing institution to verify that the transaction is legitimate. Adding a token vault into your payment infrastructure will ensure that this sensitive information is encrypted and stored securely.

2. Payment tokens and account updating

For repeat customers, card tokenization is an excellent way to solve for missing or outdated card information. By turning card details into tokens, not only do you add a layer of security and protect the customer’s sensitive card information from exposure, you also don’t have to worry about outdated information as this is updated whenever the account is updated.

Tokenization is also useful in case a repeat customer doesn’t have their card at hand: Their details are safely stored in a token vault in an encrypted form, so that the next time they want to initiate a purchase, all they have to do is click – the re-entering of card information isn’t required.

Payment tokens help to reduce friction and declines in the payment flow, so that payments are authorized quickly and seamlessly.

3. Alternative payment methods (APMs)

If the card information is inaccessible or cannot be provided, then it’s smart to offer alternative payment methods so that the customer can still complete their transaction. Including a variety of payment methods has been shown to increase conversion rates by up to 30%, and offering locally preferred payment methods are especially effective. Digital wallets make the most sense for purchases with lower average order values; for high order values, direct debit type of payment methods are the most effective.

How to solve for fraud declines

Whether it is a real fraud attempt or just a false positive, fraud declines can get in the way of payment authorizations in the short and long term, as too many failed authorizations or chargebacks will likely result in penalties from the financial institutions you work with. Here are a few ways in which merchants can prevent fraud declines.

1. Fraud prevention tools

Consider implementing a machine learning or AI-based fraud prevention tool that can automatically detect fraud and send you real-time notifications. Solutions like Ravelin, Forter or Sift to help detect fraud before the payment authorization stage. To decrease fraud in the long term, consider a post-payment fraud prevention company like Ethoca that helps merchants implement fraud prevention strategies and perform proactive refunds on guaranteed fraud cases to avoid having to pay the chargeback fees.

2. Lower risk payment methods

Lower risk payment methods like digital wallets are smart choices for fraud prevention for several reasons. First, they don’t have reversals, which means initiating a chargeback on them is not possible, taking away the ability to commit chargeback fraud. Secondly, digital wallets like Apple Pay and Google Pay use two factor authentication – a biometric face or fingerprint scan or inputting of a PIN – which can make it much more difficult for these payment methods to be stolen and used by fraudsters. And because of this two factor authentication, digital wallets tend to have higher acceptance rates.

Increase your payment authorization rates with the Payrails payment operating system

Payrails offers an all-in-one payment solution that empowers merchants to create customized payment flows that result in increased authorization rates and fewer declined payments. With Payrails, merchants only have to integrate one software layer to be immediately connected to multiple PSPs and payment methods.

Dynamic payment routing

Increase your payment authorization with Payrails’ dynamic payment routing, which automatically sends transactions along a route that has the highest authorization rates for your preconfigured conditions.

Automatic retry

Payrails’ operating system includes a retry engine that operates automatically in the background, recovering failed transactions without the need for manual intervention. Define conditions, attempts, and frequency of payment retry attempts based on the needs of your business to maximize the recovery rate. This increases authorization rates and reduces churn by providing an excellent customer experience.

Payment methods

Through our software layer, merchants can connect to multiple different global and local payment methods without having to integrate them all separately. Local payment methods usually have higher authorization rates and are more popular among the local customer base.

PSP agnostic token vault

The Payrails token vault is PSP-agnostic, meaning that the tokens it issues are valid across all PSPs. This increases security and reduces friction in the entire payment process, but especially for repeat and recurring transactions, as the card information is automatically updated by the integrated card account updater.

Analyze your declines

With our built-in payment analytics tool, you can analyze and understand which types of card declines occur the most frequently and for what reasons. This knowledge, along with the tool’s actionable insights feature, will help you to choose which of the above solutions to integrate into order to reduce payment failures and increase payment authorizations across the board.

Contact us for a customized consultation

Regardless if you’re experiencing soft declines or hard declines, Payrails can help you to reduce payment failures and increase payment success. Our modular payment operating system empowers you to design payment workflows that increase authorizations and help you meet your revenue goals. Build checkout experiences that your customers will love – get in touch today to learn more.

I am the text that will be copied.