Tokenization in payments has become fundamental to PCI compliance and performance across regions, but who controls the payment token matters more than most merchants realize.

When your PSP owns your tokens, they own your flexibility. Need to switch processors? Start tokenizing from scratch. Want to optimize routing across multiple PSPs? You're limited to whatever retry logic your primary processor allows. Planning to expand globally? Your PSP's tokens don’t always work seamlessly across all your target markets.

Merchant-owned payment token vaults flip this dynamic. Instead of storing tokenized card data in your PSP's system, you control the vault infrastructure. Your tokens become portable assets that work across any processor, region, or payment method. Your retry logic becomes sophisticated orchestration instead of basic fallbacks.

The difference is strategic. PSP-owned tokens create vendor lock-in that limits growth, while merchant-controlled payment vaults enable the flexibility that scales with your business.

What is a payment vault?

A payment vault is a PCI-compliant system that stores tokenized card data independently of any payment service provider (PSP), allowing merchants to reuse payment tokens across processors, regions, and payment methods.

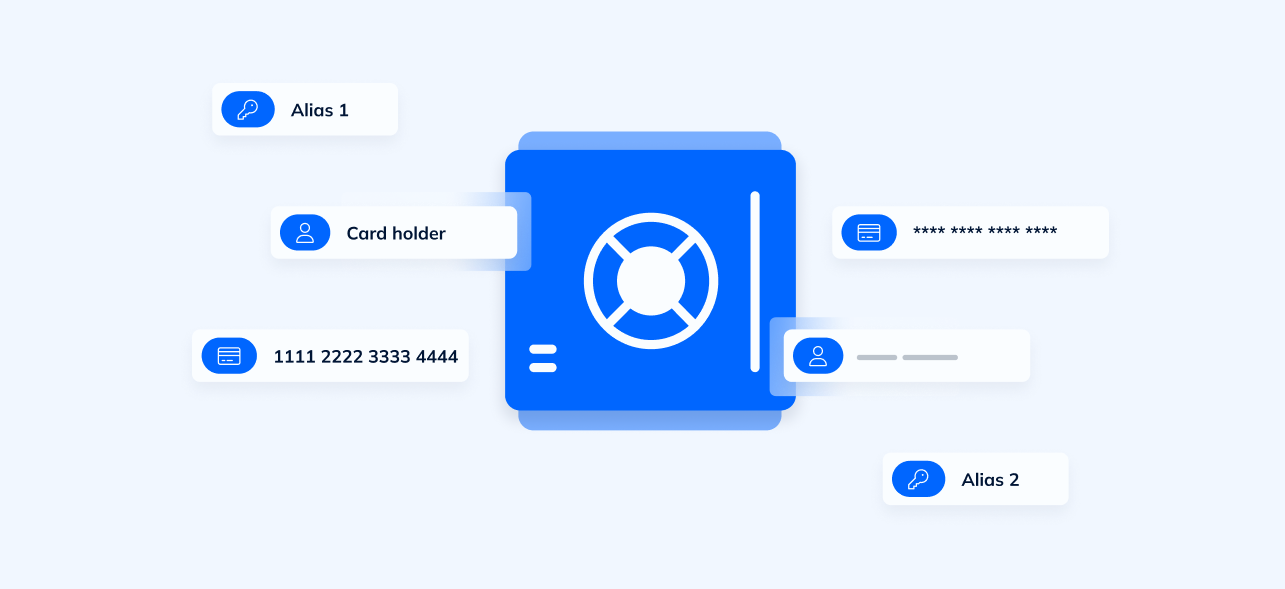

A payment vault is a secure, PCI-compliant environment that stores and manages tokenized card data independent of any specific PSP. Think of it as building your own token cloud across regions and providers.

Unlike PSP tokens that live within your processor's infrastructure, a merchant-owned payment vault gives you direct control over how sensitive payment data gets stored, accessed, and used. When a customer saves their payment method, the card vault generates a unique token that represents their card data across your entire payment ecosystem.

Payment vaults operate through a simple but powerful process:

- Card data capture: Customer payment information flows into the payment vault through secure collection methods that maintain PCI compliance without exposing your systems to sensitive data.

- Tokenization: The vault replaces actual card numbers with unique, meaningless tokens that can be safely stored and transmitted across your payment infrastructure.

- Secure detokenization: When processing payments, the vault converts tokens back to real card data only at the moment of transaction, ensuring detokenization happens within the compliant environment.

- Payment orchestration: Your tokens work across processors, enabling dynamic routing, retries, and fallback strategies – all without re-tokenizing customer data.

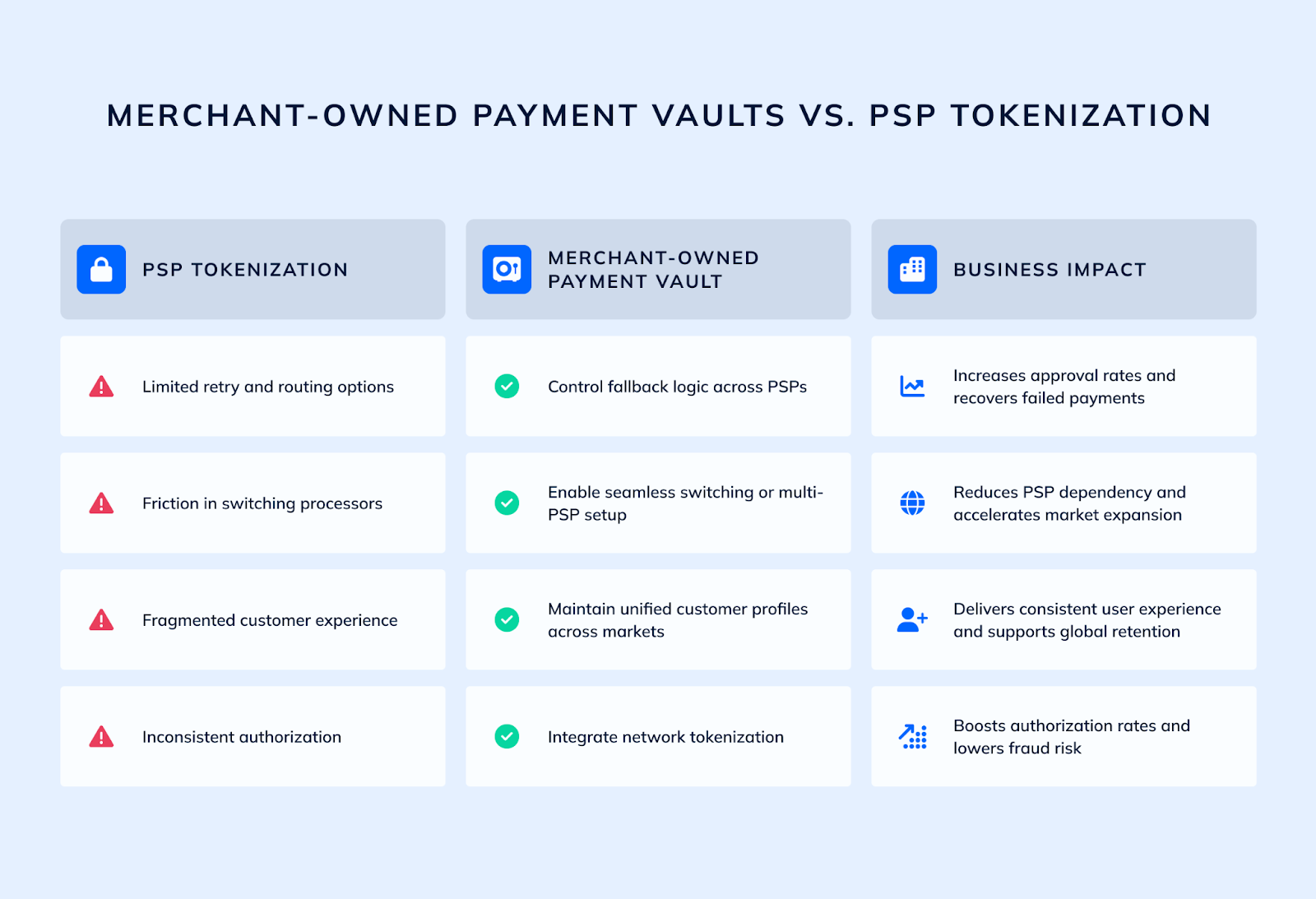

Why PSP-owned tokenization limits merchant flexibility

PSP tokens simplify initial integration but create hidden constraints that limit long-term flexibility and performance. When your processor owns your tokens, they also control your strategic options, leading to a number of potential challenges.

Limited retry and routing options

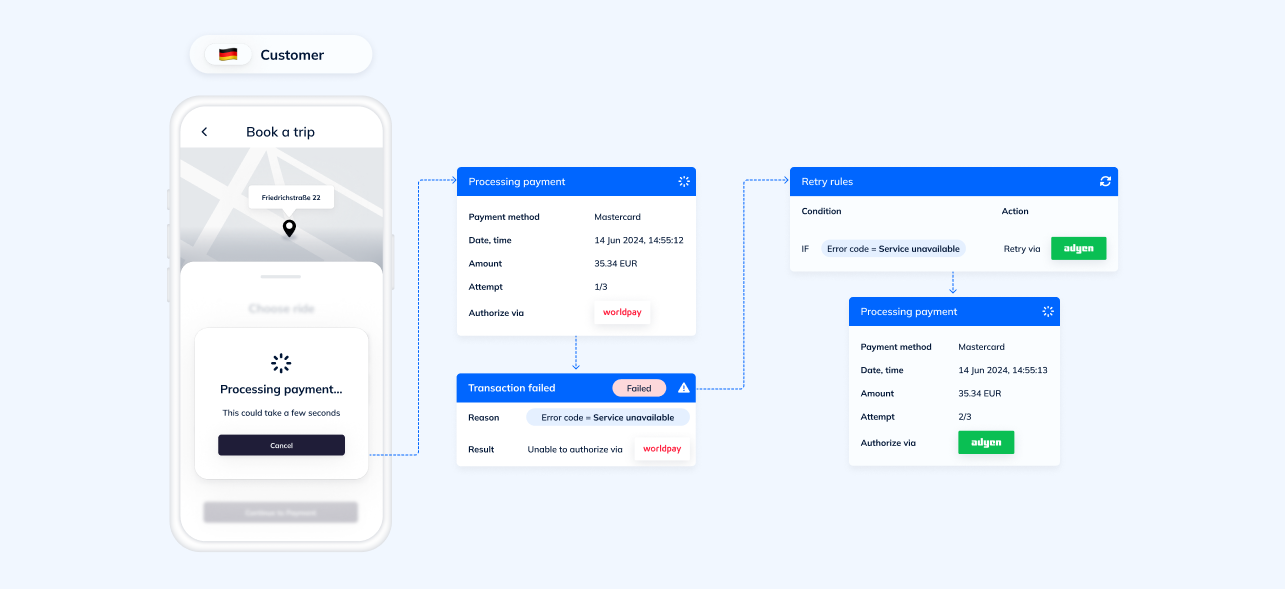

As a merchant, PSP-dependence restricts your options when it comes to handling failed transactions. If a recurring paymentfails, you're limited to whatever retry strategy your PSP allows. Advanced routing based on card type, issuer, or transaction characteristics becomes impossible when tokens only work within one processor's ecosystem.

Friction when switching PSPs

Changing PSPs requires starting your tokenization strategy from scratch. Every card on file customer needs to re-enter their payment information. Subscription businesses face massive churn during PSP migrations. Enterprise merchants lose years of carefully built customer payment profiles.

Fragmented customer payment profiles

Multi-PSP strategies become operationally complex when each processor manages separate token databases. Customer payment profiles fragment across systems. Recurring payments might work differently depending on which PSP processes the transaction. Unified reporting becomes impossible when customer identifiers vary by processor.

Inconsistent authorization performance across PSPs

PSP tokens can't leverage cross-processor authorization data for optimization. If “PSP A” has better authorization rates for European cards but “PSP B” performs better for US transactions, you can't easily route based on these patterns when tokens are locked to specific processors.

Research shows that merchants using multiple payment service providers can optimize authorization rates and reduce costs, but PSP-owned tokenization limits this flexibility.

Benefits of merchant-owned payment vaults

As enterprises grow, optimizing payments across multiple providers becomes essential for performance. One Payrails merchant processing over 5 million payments per month saw a 6% uplift in authorization rates and a 10% reduction in payment-related churn after adopting PSP‑agnostic tokenization and smart routing. It’s a clear example of how merchant-owned vaults and intelligent payment infrastructure translate directly into business results.

What else makes merchant-controlled payment vaults such a powerful enabler of payment strategy? Here’s how they help businesses adapt at scale – without being held back by PSP constraints.

Control fallback and retry logic across PSPs

With a merchant-owned vault, failed transactions can be retried across multiple processors using intelligent routing rules. If “PSP A” declines a transaction, the same payment token can immediately retry through “PSP B” without requiring customer re-authentication. This can significantly improve transaction recovery rates by enabling intelligent retry strategies across multiple processors.

Advanced retry logic considers card type, issuer response codes, transaction amount, and historical performance patterns. Recurring payments benefit from sophisticated timing strategies that optimize authorization rates based on customer-specific data rather than generic PSP defaults.

Unified customer payment profiles across regions

Card vault infrastructure enables consistent customer experiences across regions and processors. A customer's payment token works whether they're processed through your European acquirer, Asian gateway, or North American PSP. Their payment profile remains unified regardless of which processor handles the transaction.

This consistency extends to recurring payments where subscription businesses maintain seamless billing cycles even when routing transactions through different processors for cost or performance optimization.

Seamless PSP switching and multi-PSP setups

Merchant-owned vaults eliminate the switching costs that create PSP lock-in. Adding new processors becomes a configuration change rather than a customer migration project. Payment tokens remain valid across any processor integration, enabling gradual transitions or sophisticated routing strategies. Merchants can route transactions based on cost, performance, or regional requirements without fragmenting their customer database or requiring multiple tokenization integrations.

For merchants seeking to increase payment authorization rates and revenue through more efficient routing, multi-PSP strategies are an important building block. They become significantly easier to implement when customer card data lives in a centralized payment vault.

Network token integration with card networks

A merchant-owned payment vault can integrate with network tokenization from Visa, Mastercard, and other card networks. Network tokens from major card networks often deliver higher authorization rates and reduced fraud compared to traditional PANs, while remaining portable across any processor that supports network tokenization.

With Payrails, network tokens can be deployed as part of a merchant-owned vault, used independently across PSPs, or combined with orchestration to enable smart retries, dynamic routing, and fallback. This flexibility gives merchants full control over how and where tokens are used, keeping payment setups and business priorities aligned.

Research from Visa shows that businesses using network tokens see an average 4.6% increase in authorization rates for card-not-present transactions, while reducing fraud by up to 30%. Payrails’ merchant data further demonstrates the value: merchants combining network tokens with orchestration achieved up to a 43% uplift in authorization rates and a 93% reduction in avoidable declines.

The combination of merchant-controlled vaulting, cross-PSP compatibility, and orchestration unlocks one of the most flexible and high-performing tokenization strategies available today.

PCI compliance, with a lower burden

Beyond flexibility and performance, merchant-owned payment vaults also simplify PCI DSS 4.0 compliance by reducing overall audit scope.

Merchant-owned vaults play a key role in PCI DSS 4.0 Level 1 compliance by reducing overall audit scope and regulatory burden.

Tokenization helps organizations reduce the scope of their PCI DSS compliance requirements by replacing sensitive card data with tokens, allowing businesses to allocate fewer resources to compliance audits while saving time and money.

When tokenized, information no longer contains cardholder data and does not fall within the scope of PCI DSS, making tokens widely considered a safe way of storing and transmitting sensitive information.

Putting the token vault back in the hands of the merchant minimizes sensitive data exposure across your entire payment infrastructure. Instead of card data flowing through multiple systems, only tokens move through merchant environments. Detokenization happens only within the compliant vault infrastructure at the moment of payment processing.

Vault proxy architecture

Payrails' Vault proxy design helps merchant systems minimize PCI scope while providing full control over payment tokens. The proxy pattern ensures sensitive card data never touches merchant infrastructure, even during detokenizationprocesses.

This architecture enables PCI scope reduction by minimizing the systems and processes that require PCI compliancevalidation. Merchants gain token control without expanding their regulatory footprint.

Simplified audit processes

Centralized payment vault infrastructure often simplifies PCI DSS audits compared to distributed tokenization across multiple PSPs. Single-source compliance documentation, unified security controls, and consistent audit procedures reduce the complexity of maintaining PCI compliance across global operations.

Reduced integration complexity

Merchant-owned vaults eliminate the need to maintain PCI compliance for multiple PSP tokenization integrations. Instead of ensuring compliant handling of card data across numerous processor APIs, merchants interact only with their payment vaultthrough standardized, token-based interfaces.

Payrails’ merchant-owned token vault advantage

Payrails token vault and vault proxy offer enterprise-grade performance, flexibility, and PCI DSS 4.0 Level 1 compliancedesigned to scale with sophisticated payment infrastructure requirements.

Key capabilities include:

- Universal token compatibility: Works seamlessly with PSP tokens, network tokens, and proprietary tokenization schemes. Migrate existing tokens or implement new tokenization strategies without disrupting current payment flows.

- Secure detokenization flows: Detokenization happens through secure proxy patterns that helps merchant systems reduce PCI scope while enabling real-time payment processing across any integrated PSP or gateway.

- Card updater integration: Automatic card updater services ensure recurring payments continue seamlessly when customer cards expire or get replaced. Token updates propagate across all systems without customer intervention.

- Cross-PSP orchestration: Single payment tokens work across unlimited PSP integrations, enabling sophisticated routing, retry, and fallback strategies that optimize for cost, performance, and authorization rates.

- Network tokenization support: Native integration with Visa, Mastercard, and other network token programs delivers enhanced authorization rates and fraud protection while maintaining full portability.

- Real-time performance monitoring: Analytics track token usage, authorization rates, and recurring paymentperformance across all PSPs and regions, enabling data-driven optimization of payment orchestration strategies.

- Global compliance coverage: PCI DSS 4.0 Level 1 certification with support for regional compliance requirements, including GDPR, CCPA, and other data protection regulations.

The payment orchestration platform integrates with existing payment infrastructure or operates standalone, enabling gradual migration from PSP tokenization to merchant-controlled vault strategies without business disruption.

How to transition from PSP tokenization to a merchant-owned vault

Moving from PSP tokenization to a merchant-controlled payment vault doesn't require a wholesale infrastructure overhaul. The smartest approach starts with understanding your current state, then builds incrementally toward full payment orchestration capabilities.

Start with a strategic assessment

Before implementing any new tokenization strategy, you need a clear picture of your current payment ecosystem and its limitations. This assessment phase reveals both the immediate opportunities and potential obstacles for merchant vault adoption.

- Audit existing tokenization: Document which PSPs currently manage your payment tokens, how many card-on-file (CoF) customers you have per processor, and where token limitations create operational constraints.

- Identify switching costs: Calculate the customer impact and revenue risk of PSP migration under current PSP tokenization models.

- Map customer journey friction: Track where PSP-dependent tokenization creates suboptimal customer experiences, particularly in recurring payments, cross-border transactions, or multi-channel commerce.

Complicated payment flows are a leading cause of churn, abandonment, and revenue loss, much of which could be avoided with smoother payment flows. Research has shown that subscription SaaS businesses lose 14% of revenue and 13% of their customers annually to churn.

Design your routing strategy

With your current state mapped, the next step involves defining how merchant-controlled tokenization will improve payment performance and customer experience. This strategic design phase determines the specific benefits your payment vaultimplementation will deliver.

- Analyze failed transaction patterns: Identify which transaction types, card brands, or regions have suboptimal authorization rates that could benefit from multi-PSP retry strategies.

- Design routing logic: Specify how payment tokens should route across PSPs based on cost, performance, and authorization rate optimization.

- Plan recurring payment optimization: Determine how merchant-controlled tokenization can improve subscription billing success rates and reduce involuntary churn.

Prepare for implementation

The technical and compliance preparation phase ensures your merchant vault deployment succeeds without disrupting existing payment operations or expanding regulatory burden.

- Assess current compliance footprint: Document existing PCI compliance scope across all systems that currently handle card data or PSP tokens.

- Plan scope reduction strategy: Identify opportunities where payment vault proxy architecture can remove systems from PCI scope while improving token functionality.

- Validate integration requirements: Ensure technical teams understand how vault integration differs from direct PSP tokenization and plan development resources accordingly.

Validate your approach

The final preparation step involves seeing payment vault capabilities in action with your specific data and use cases. This validation phase confirms implementation feasibility and quantifies expected benefits.

- Review vault capabilities: See how Payrails’ Token vault handles secure detokenization, cross-PSP orchestration, and PCI compliance for your specific use cases.

- Test token migration: Payrails provides comprehensive documentation and migration tools that typically enable seamless token portability without customer re-authentication.

- Plan implementation timeline: Deployments are typically delivered faster than building and certifying an internal vault – often in just a few months.

Own your token infrastructure, control your growth

Payment vaults are strategic assets enabling payment flexibility, performance optimization, and business growth without vendor constraints.

PSP tokenization might seem convenient initially, but the hidden costs of lock-in, limited retry logic, and fragmented customer data compound over time. Merchant-owned payment vaults require more thoughtful implementation but deliver exponentially greater long-term value.

Ready to take control of your payment tokens? Contact Payrails to see how our Token vault can transform your payment infrastructure.

I am the text that will be copied.