A chargeback is a transaction reversal initiated when a cardholder disputes a charge. Managed by the cardholder’s bank under card network rules, the chargeback process exists to protect consumers – from fraudulent use, goods not received, duplicate charges, or credits not processed – but it can be tough on merchants. For large enterprises running multiple PSPs and channels, the experience becomes even more challenging.

There’s no getting around the fact that chargebacks are an inconvenience. Funds are pulled. Strict deadlines start immediately. Evidence standards vary by bank and network. Merchants who don’t resolve chargeback disputes in a timely fashion face onerous charges and escalating fines from the card networks. Fees pile up even if you ultimately win.

How can merchants make the process more manageable? By treating chargebacks as an analytics and operations challenge which can be measured, improved and optimized.

This article breaks down the full chargeback lifecycle, shows how to build AI-tailored representments on top of unified data, and explains which KPIs actually guide action by bank and region. You’ll also see how to prevent disputes with pre-dispute notifications, how to streamline evidence gathering so submissions land on time, and how to connect dispute outcomes to settlements and fees so Finance can close faster.

The chargeback lifecycle, step-by-step

Every chargeback dispute follows a predictable path. When teams understand the stages and who owns each one, you stop losing cases to preventable errors and shorten time to resolution.

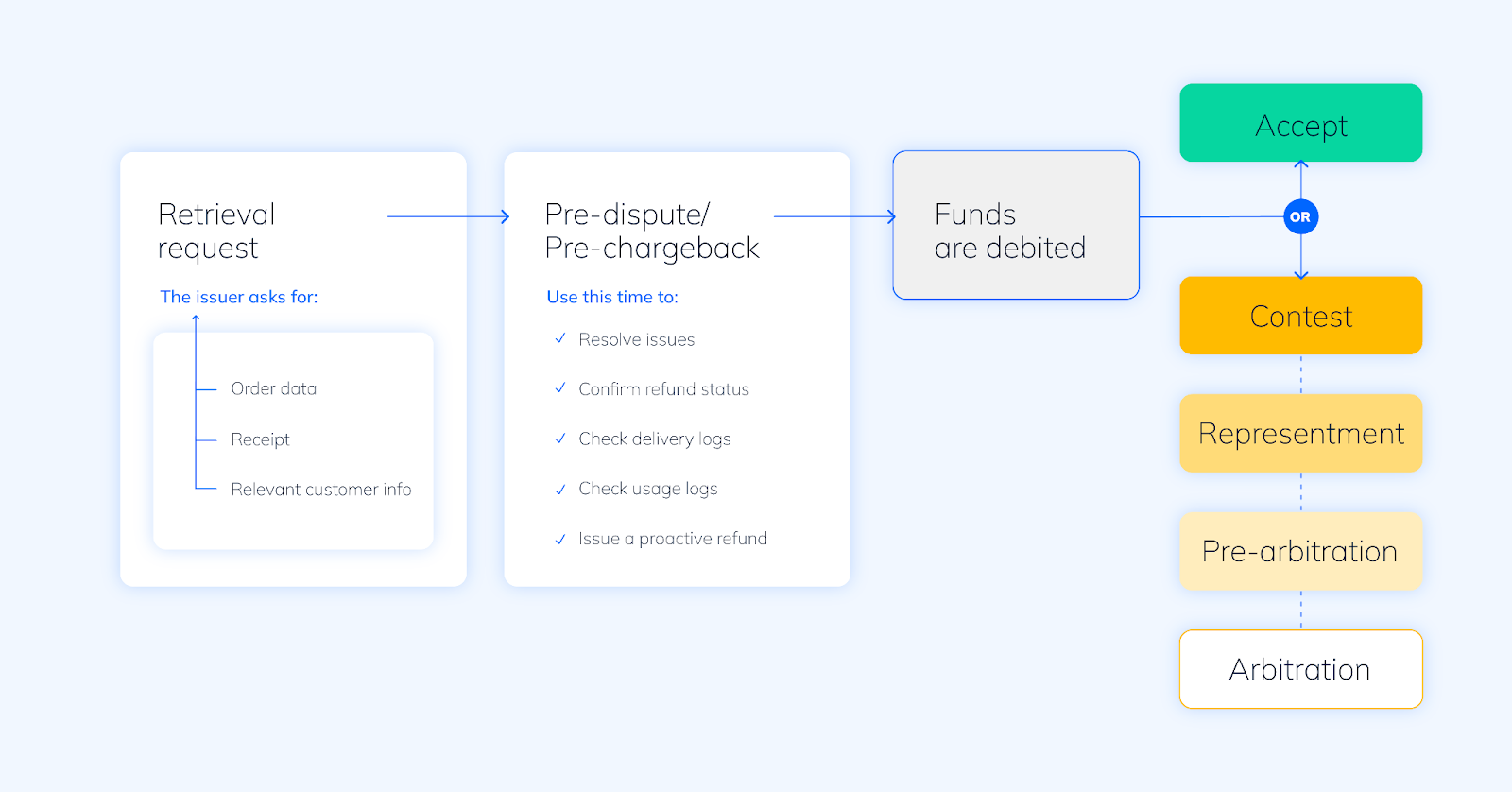

The process typically starts with a retrieval request (request for information). The issuer asks for details before filing a formal chargeback. Respond promptly with order data, a receipt, and relevant customer communications. Set a short internal SLA so your team builds the habit of fast replies, as quick information can help to defuse a complaint.

Next is pre‑dispute or pre‑chargeback – an early warning from the network or issuer. Use this time to resolve the issue before funds move. Confirm refund status, check delivery and usage logs, and issue a proactive refund when the evidence supports the customer.

If the case progresses, the first chargeback arrives and funds are debited. It’s now up to you to decide whether to accept the loss or fight it formally. If you contest, the process goes to representment – a formal response with supporting evidence that maps directly to the reason code and shows how the transaction was authorized, fulfilled, and communicated.

After representment, the issuer may open pre‑arbitration for another review, and some cases escalate to arbitration, where the network makes a final decision. Escalation is costly, so continue only when value and win probability justify it.

Documenting these stages in a clear playbook helps teams act quickly and consistently, even when volumes spike. But knowing the steps alone isn’t enough – enterprises also need to measure how well they’re performing at each stage. That’s where tracking the right KPIs becomes essential, giving managers the visibility to spot bottlenecks, compare issuers, and improve outcomes over time.

KPIs and dashboards that matter

When it comes to the chargeback process, one of the benefits of a unified analytics dashboard is to help merchants identify where to act first.

Here are some of the main data points to keep an eye on:

- Your chargeback rate is the main anchor. Track disputes as a share of transactions or total payment volume by month and cohort. Spikes in one market usually point to a product or policy issue, not a global problem.

- Win rate shows how well operations convert effort into outcomes. Break it down by reason code, issuer, and region. If win rate is low for a single issuer, it might indicate that your submissions may not meet their preferences. If it is low for one code, it’s a sign that you may need to strengthen your narrative and exhibits during representment.

- Time‑to‑submit measures how quickly you meet representment deadlines. Shorter cycles help you avoid missed deadlines and chargeback backlogs which can compromise your ability to respond to new disputes.

- Track TPV impact and fee recovery so Finance sees materiality and ROI.

Payrails provides KPI dashboards with provider/country/issuer filters and CSV/API exports for recurring reports. Weekly reviews keep teams aligned and help surface spikes early.

Tip: Start with a small set of metrics and drill down by issuing bank, country, and PSP to expose outliers you can fix quickly. Your unified analytics dashboard is a good way to identify recurring patterns with specific issuing banks or card networks.

Looking for a quick win? Find the five issuers driving the most losses, and see if there are any underlying patterns that can be addressed.

Build the data foundation: Unifying and normalizing payments data

Winning disputes requires complete context. Most merchants have data spread across PSP portals, ticketing, order management, shipping, and data warehouses. When managing chargebacks, start by pulling the data into one place – and then normalize it so that every case starts with the same foundation.

- Connect to your major PSPs to import chargeback events, notifications, settlement adjustments, and dispute outcomes. Add order and customer records so evidence matches the purchase.

- Create a standardized taxonomy for disputes and declines. Providers often label reason codes differently – map them onto a common schema so that your analysis can compare like-for-like. If “no cardholder authorization” disputes spike with one issuer in one market, investigate 3DS coverage, device fingerprint consistency, or descriptor clarity for that segment.

- Link entities so each dispute ties to its order, authorization result, risk signals, shipment or delivery confirmation, and refund events. This thread is your story and should be reviewable in one single view.

- Close the loop with reconciliation. Tie disputes to settlements and fees so that your finance department can validate recoveries and avoid month‑end surprises. When analytics match bank statements, your CFO will have an easier time trusting the overall process.

Payrails combines connectors, standardized taxonomies, and reconciliation that links disputes to settlements and fees. Every case starts with the full picture, and every report matches financial reality.

Evidence that wins: AI‑tailored representment, with guardrails

For years, merchants have relied on static reason code templates to respond to chargebacks. These templates helped standardize responses, but they quickly break down at scale. Issuers don’t all want the same proof. Networks update requirements often. And with high dispute volumes, teams spend hours copy-pasting screenshots and logs, only to see inconsistent outcomes.

AI-assisted representment changes the game. Instead of relying on one generic template, merchants can generate tailored dispute packages that reflect the issueahr, scheme, region, merchant policy, and specific reason code. Each pack is built from the full context of the transaction, then routed through a controlled review to ensure accuracy and compliance.

Here’s how merchants can streamline representment using AI, and what goes into making it work.

- Begin with data assembly. Gather order details, authorization outcomes, device and session signals, delivery or usage logs, customer communications, refunds, and settlement references. Because the taxonomy is normalized, the model understands the reason code and expected evidence.

- Inject policy and scheme rules through a structured checklist that reflects network requirements and known issuer preferences. For physical goods, prioritize signed delivery and tracking milestones. For digital goods, use login history and device continuity. Include refund, cancellation, SCA/3DS configurations, and local regulations to keep responses consistent with practice.

- Next, the LLM produces a draft narrative that explains the transaction from authorization to delivery, maps exhibits to the reason code, and cites source records by ID and timestamp. It assembles screenshots and confirmations, applies automatic PII redaction, and exports in the format preferred by the scheme.

- Keep a human‑in‑the‑loop step. Reviewers validate facts, add missing context, and sign off. Store the final pack immutably with a version history and log every prompt, input, and output for audit.

- Close the loop with learning. Record outcomes by issuer and reason code. Feed features such as evidence completeness, timeliness, and narrative clarity back into prompts and checklists. Each cycle improves the next.

Governance matters. Enforce clear access to case data, use redaction by default, limit free‑text insertion, and require approvals for any step that touches raw payment credentials. These guardrails let you scale AI assistance without creating new risks.

The net effect is faster time‑to‑submit, higher first‑pass acceptance, and a steady improvement in win rate where it matters most.

Operate faster: SLAs, alerts, and anomaly detection

One of the most frustrating parts of chargebacks is losing cases not because the evidence was weak, but because the team missed a deadline or didn’t notice a sudden spike in disputes. A strong case can still be written off if it sits in the wrong queue over a weekend, or if no one notices that inflow doubled with a single issuer until it’s too late. For merchants, these operational misses are preventable – and fixing them often has a bigger impact on win rate than rewriting policies.

The answer is to bring more structure and visibility into dispute operations. That means setting response targets (SLAs) that are tighter than scheme rules, automating alerts so nothing slips through, and watching for unusual spikes so the team can act before small problems turn into trends.

Tips:

- Set internal SLAs that are tighter than the limits enforced by card schemes. Respond to retrieval requests within 48 hours and aim to submit representment well before the cutoff. Publish targets on dashboards.

- Maintain a shared queue with a named owner for each case. During peaks, rotate on‑call coverage so work doesn’t stall. Managers should see backlog age, time‑to‑submit, and breach risk at a glance and reassign work quickly.

- Add anomaly detection. Alert when inflow jumps above a rolling baseline, when one issuer breaks pattern, or when a region deviates from trend. Early alerts enable quick fixes – descriptor updates, targeted credits, or product changes – before complaints become disputes.

Merchants that run disputes this way keep cases moving, meet deadlines reliably, and free managers to focus on exceptions rather than firefighting.

Prevention first: Reduce inflow at the source

For merchants, the most frustrating chargeback is the one that could have been avoided entirely.

Many disputes don’t stem from fraud at all – they start as confusion or poor communication. A shopper doesn’t recognize a billing descriptor, can’t find a refund confirmation, or gets tired of waiting for a support reply. What might have been solved with a quick email or refund turns into a full chargeback, complete with fees and lost time.

That’s why the best chargeback strategy begins with prevention. Merchants can reduce inflow in two ways:

- Fix the basics so fewer customers ever feel the need to dispute.

- Use pre-dispute alerts to solve the customer's problem quickly, resulting in fewer chargeback proceedings.

Track 1: Strengthen the fundamentals

- Use a clear, recognizable statement descriptor. Include a URL or phone number.

- Process refunds quickly. It’s cheaper than handling a full dispute.

- Apply SCA/3DS intelligently. Use exemptions for low-risk cases, step up for higher-risk.

- Keep customers informed. Send receipts, shipping updates, and renewal reminders.

- Security makes a difference. Use signed delivery for high-value goods and login or device logs for digital content.

Track 2: Deflect complaints with scheme alerts

- Connect to issuer alert programs. Platforms like Ethoca and Verifi help you see complaints before they hit as chargebacks.

- Auto-refund low-value or clear-cut cases. Identify which cases don’t make sense to challenge.

- Stay on top of legitimate orders. Send enhanced details (items, delivery, usage) back to issuers so they can reassure cardholders.

- Prioritize cases. Apply a simple decision model that weighs order value, shipment status, and customer history.

- Identify fraud when it’s obvious. Cancel fulfillment or revoke access when patterns strongly suggest fraud.

Operationalizing prevention

To make prevention stick, merchants need to move beyond ad-hoc fixes and build prevention into their daily operations. That means making sure alerts flow automatically into existing systems, adding the right order and payment context so decisions can be made quickly, and keeping records in sync across PSPs and CRM tools.

Just as importantly, merchants should measure the results. How many alerts were resolved before turning into chargebacks? How much revenue was saved? How fast were teams able to respond? Tracking these outcomes alongside acceptance and fraud rates shows whether prevention is truly reducing both disputes and cost – and what kind of an impact this is making on your overall bottom line.

Finance impact: Recover fees and close faster

For many merchants, chargebacks are seen as an operations problem, but the financial impact is just as painful. Revenue is lost the moment funds are pulled, fees stack up even if cases are won, and unsettled disputes stretch out cash cycles. Finance teams often struggle because the data they need sits in different places, making it hard to see the true impact or justify investments in prevention.

The fix is to tie dispute operations back to financial reporting. By regularly reporting on recovered revenue, tracking settlement deductions, and showing how long funds remain outstanding, Finance gains visibility into how disputes affect cash flow.

To make these reports actionable, finance teams can focus on a few concrete data points:

- Track recovered revenue. Show how much was won back through representment or proactive resolution, broken down by issuer or region.

- Monitor settlement deductions. Flag when and how much was pulled, and measure the average time until funds are restored.

- Calculate fee recovery. Compare fees refunded on wins with those avoided through prevention or early deflection.

- Measure DSO impact. Track how long disputed amounts remain outstanding and how improvements shorten cash cycles.

- Break down by issuer and reason code. Identify the banks or dispute categories causing the most loss and prioritize fixes.

Platforms such as Payrails support this by reconciling disputes directly to settlement lines and fees, and by providing ERP/BI exports that reduce manual month-end work. This ensures Finance and Operations stay aligned and progress is measured in terms that drive business decisions.

Payrails: One operating system for disputes and analytics

During the chargeback process, most enterprises need more than a tool that just submits evidence – they need a system that unifies data, standardizes how evidence is created, and connects dispute outcomes back to payments and settlements.

Just as importantly, they need insights by issuer, provider, and country so they can reduce inflow at the source, not just respond faster.

That’s where Payrails comes in – providing a true payment operating system to help you experience fewer chargebacks, prioritize the ones that matter most, and win the cases that are worth pursuing:

- A unified analytics layer that pulls in PSP and regional data into one view.

- Configurable workflows with ownership, SLAs, and reminders to keep cases on track.

- Evidence packs generated from normalized reason codes and linked order/settlement data, ready for AI-assisted drafting and human review.

- Reconciliation that ties disputes back to settlements and fees.

- Access and activity logging for compliance and audit confidence.

The result is faster operations, more consistent outcomes, and fewer surprises at audit time.

Looking for a way to reduce chargeback costs, improve win rates, and restore predictability to both operations and finance?

See how Payrails can transform your approach to chargebacks.

Conclusion and next steps

For most enterprises, chargebacks feel like a tax on doing business: unpredictable, costly, and disconnected from the rest of payments. But it doesn’t have to be this way. With the right data and processes, disputes can be managed like any other part of your business operations – measured, optimized, and steadily improved.

Clear metrics, repeatable evidence, and unified analytics turn chargebacks from a black box into something predictable. Instead of scrambling at deadlines, teams can respond with confidence, finance departments can forecast cash impact, and leaders can see where to invest for long-term gains.

To start building that foundation:

- Connect providers and baseline KPIs in a single dashboard.

- Map owners and SLAs to each lifecycle stage, and enable alerts.

- Pilot AI-assisted representment for one high-volume reason code and your top issuers.

- Turn on scheme alerts and define auto-refund thresholds.

- Reconcile disputes to settlements so Finance can close faster.

Chargebacks may never disappear, but they can stop being a constant drain. With the right operating system in place, merchants win more, lose less, and regain control over both revenue and time.

FAQs

What is the chargeback cycle?

In payments, the chargeback cycle is the process by which chargeback disputes are settled. The chargeback cycle begins when a cardholder disputes a transaction with their issuing bank. The issuer may first send a retrieval request (a request for information) to the merchant. Many networks also send pre-dispute alerts that give merchants an early chance to resolve the complaint. If the matter continues, a first chargeback is filed and funds are debited from the merchant. The merchant can respond with representment, a structured package that explains why the charge was valid and includes evidence. Some cases proceed to pre-arbitration for another review, and a small number reach arbitration, where the card network makes a final decision. Each step has strict timelines.

How do I improve chargeback win rate?

Merchants can improve their chargeback win rate through responses that are complete, consistent, and on time. Effective teams assign owners, set internal response-time targets, and submit a single, well-organized package that matches the reason code (a specific identifier assigned to transactions that fail or require further examination). When challenging a chargeback, the merchant’s narrative should be short and clear, supported by order data, authorization results, delivery or usage proof, and customer communications. After decisions, merchants review results by issuer and reason code to learn what each bank expects and adjust future submissions accordingly.

Which evidence is required for representment?

Evidence varies by reason code and circumstance, but strong submissions usually include: order and payment details (amount, date, items, and device/IP; AVS/CVV or 3DS result if used), fulfillment or usage proof (tracking and delivery confirmation for physical goods; login/download/access logs for digital goods), customer communications (emails or chats, refund requests, and confirmations), and policies shown at checkout (refund policy, terms and conditions, and the statement descriptor as displayed). All files should have clear timestamps and legible screenshots, with unnecessary personal data redacted. A brief cover note should explain how each exhibit addresses the reason code.

How can merchants unify chargeback data and evidence across multiple PSPs?

To unify chargeback data, merchants can connect APIs or exports from each payment service provider (PSP) and load payments, disputes, and settlements into one store. They use a common schema and map provider-specific reason codes to a single list. Each dispute is linked to its order, authorization, shipment, refund, and any support tickets so reviewers can see the full story. Finally, disputes and fees are reconciled to settlement lines so Finance can confirm recovered amounts. Platforms such as Payrails help by providing the connectors, normalization, and reconciliation tools needed to make this process seamless.

What chargeback KPIs should payments teams track across regions?

A practical set includes chargeback rate (disputes vs. total transactions or volume), win rate (wins vs. cases contested), time-to-submit (notification to response), acceptance rate and fraud rate (reviewed together), and deflection rate (alerts resolved before becoming chargebacks). Teams also monitor issuer concentration (which banks drive losses), aging backlog, fee recovery, and days to cash recovery. Breaking KPIs down by issuer, country, and PSP helps find outliers quickly. Platforms such as Payrails provide dashboards and filters that make it easier to view these KPIs consistently across regions.

How do SCA exemptions impact chargeback rates?

Strong Customer Authentication (SCA) can reduce some fraud-related disputes, but mandatory step-up on every transaction can lower approval rates. Exemptions such as low-value, low-risk (TRA), or merchant-initiated/recurring let merchants apply step-up only when risk is higher. Results should be tracked by issuer and market to balance dispute reduction while maintaining approval rates.

What’s the difference between a retrieval request and pre-arbitration?

A retrieval request is an early information request from the issuer before a formal chargeback. For merchants, quick and clear answers can help to prevent escalation. Pre-arbitration occurs later, after representment, when the issuer challenges the outcome and seeks another review. At pre-arbitration, merchants weigh case value, potential fees, and the chance of success before deciding whether to proceed toward arbitration.

I am the text that will be copied.