A refund is a controlled process where you return a customer’s money but keep the customer relationship, avoid penalties, and limit the loss to the transaction itself. A chargeback is what happens when that same issue escalates to the cardholder’s bank. You lose the sale and pay a dispute fee. You also often lose the product, absorb processing costs, risk escalating penalties from card networks if your dispute rate climbs, and harm your brand reputation and customer trust.

Companies worldwide lost an average of 7.7% of annual revenue to fraud, equivalent to an estimated $534 billion globally. At scale, this becomes a systemic problem, with global chargeback costs projected to climb to $41.69B by 2028 from $33.79B in 2025.

Most merchants try to reduce chargebacks with one set of fixes, but that’s where things break down. When you apply the wrong solution to the wrong type of dispute, you increase costs without reducing your chargeback rate.

In this guide, we’ll break chargeback prevention into three categories – merchant error, criminal fraud, and friendly fraud – so you can focus on what actually reduces disputes.

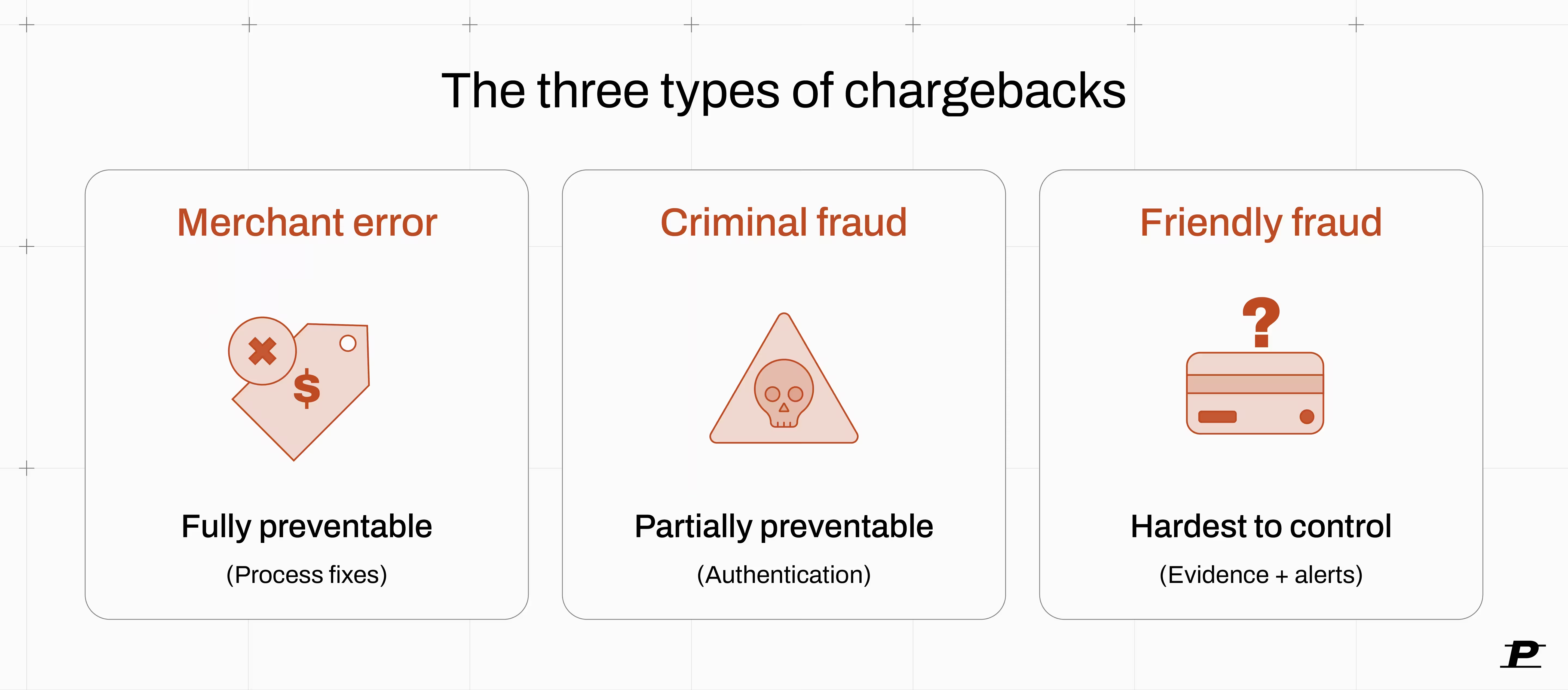

What are the three different types of chargebacks?

Chargebacks aren’t all the same. There are three categories of chargebacks, each reflecting a different underlying issue: merchant error, criminal fraud, and friendly fraud. Understanding these categories helps you target prevention efforts more precisely.

Merchant error chargebacks

Merchant error chargebacks are disputes caused by issues in your own processes. These include duplicate charges, incorrect amounts, orders that were never fulfilled, refunds that weren’t processed properly, or billing descriptors customers don’t recognize.

The most common trigger is when the name on the customer’s bank statement doesn’t match the brand they bought from. When a legal entity name appears instead of the customer-facing brand, the charge looks unfamiliar, and the customer goes to their bank.

Fortunately, merchant error chargebacks are the easiest to prevent because they’re fully within your control. Clear billing descriptors, accurate charging, reliable fulfillment, and visible support and refund flows remove most of the reasons a customer would escalate to a dispute.

Criminal fraud chargebacks

Criminal fraud (also known as third-party fraud) covers transactions made using stolen card details or compromised customer accounts. The cardholder didn’t authorize the purchase, so when the dispute is filed, the bank reverses the payment. In most cases, the merchant loses both the revenue and the goods.

This type sits in the middle in terms of preventability. You can reduce it with authentication tools like 3D Secure, AVS, CVV checks, and risk scoring, but you won’t eliminate it entirely.

It’s also the hardest to win in representment. If the cardholder didn’t authorize the transaction, the issuer almost always sides with them.

Friendly fraud chargebacks

Friendly fraud happens when a customer disputes a transaction they actually authorized. Despite the name, there’s nothing “friendly” about it for merchants. It results in the same loss of revenue, fees, and operational overhead.

In many cases, customers go straight to their bank because it’s faster than contacting support. They may not recognize the charge, forget a subscription renewal, or choose the quickest path to a refund.

This category is often underestimated. Friendly fraud is widely considered the largest category of disputes for most merchants.

How to prevent each type of chargeback

Preventing chargebacks effectively means targeting the root cause behind each type: whether it’s operational mistakes, fraud, or customer misunderstandings. The best way to go about this is to eliminate what you control first, then reduce what you can’t fully prevent.

Fix the merchant error first

Merchant error chargebacks are often caused by common operational issues that can be easily addressed by doing the following:

- Fix common transaction errors: Eliminate duplicate charges, incorrect amounts, missed refunds, and unfulfilled orders.

- Use clear billing descriptors: Match the name on the statement to your brand and include a support phone number.

- Make policies visible: Show return and refund policies at checkout, not buried in footers.

- Improve customer support: Respond quickly so customers contact you instead of their bank.

- Tighten fulfillment workflows: Send immediate order confirmations, provide tracking numbers early, and communicate delays proactively.

- Align billing with fulfillment: Capture payment when items ship, not before.

- Handle subscriptions properly: Send renewal reminders, keep pricing clear, and make cancellation easy to avoid unnecessary disputes.

Shifts liability through authentication

Criminal fraud can’t be eliminated, but it can be reduced and, in some cases, shifted away from the merchant using common authentication tools:

- Address Verification Service (AVS) checks whether the billing address entered by the customer matches the address on file with the issuer. AVS is most reliable in North America, coverage and match accuracy vary significantly across European and Asia-Pacific markets.

- CVV (Card Verification Value) verifies that the customer has access to the physical card by matching the security code.

- 3D Secure 2 (3DS2) shifts the risk calculation. Instead of the merchant making the risk decision alone, the transaction is routed to the issuer for verification. The issuer uses its own data – transaction history, device signals, behavioral patterns – to approve or challenge the transaction. When authentication succeeds, liability for fraud typically shifts from the merchant to the issuer.

Most fraud prevention systems are built on top of these checks using risk scoring. They analyze signals like device fingerprinting, IP address consistency, purchase velocity, and past behavior to identify suspicious patterns. Multiple failed attempts, mismatched addresses, or unusually large first-time purchases are common red flags.

The trade-off is false positives. The stricter your filters, the more legitimate transactions you decline. In many cases, overly aggressive rules cost more in lost revenue than they save in prevented fraud.

That’s why many merchants move to risk-based authentication. Instead of applying friction to every transaction, platforms like Payrails trigger additional verification, like 3DS, only when the risk score crosses a certain threshold. This keeps approval rates high while still reducing fraud exposure.

Alert networks and CE3.0

Not all chargebacks need to reach the formal dispute stage. Alert networks give you a window to act before that happens. Chargeback alert networks like Ethoca (Mastercard), Verifi CDRN (Visa), and Visa RDR give merchants a 24–72 hour window to resolve disputes before they formalize.

For disputes you do fight, Compelling Evidence 3.0 (CE3.0) from Visa improves your chances in friendly fraud cases (reason code 10.4 in the US). To qualify, you must match the disputed transaction to two prior undisputed transactions using at least two of four data points: User ID, IP address, shipping address, or device ID.

This requires consistent data collection across systems. For merchants using multiple PSPs, platforms like Payrails help centralize this data so it can be used effectively in dispute responses.

Pre-shipment warning signs

Friendly fraud often shows signals before the order is fulfilled. Catching these early lets you intervene before the dispute happens. Common patterns include:

- Mismatched names between the cardholder and the shipping recipient

- Multiple failed payment attempts

- Inconsistencies between billing and shipping postal codes

- High-value first orders, especially when combined with expedited shipping to a new address

- Subscription behavior, such as customers canceling immediately after the first fulfillment

Individually, these signals aren’t proof of fraud. Together, they indicate higher dispute risk.

At low volume, you can review these orders manually before fulfillment. At scale, patterns should be identified through data collection and anomaly detection, allowing you to flag risky orders without slowing down legitimate ones.

What happens when your chargeback rate gets too high

Even well-run merchants see spikes in their chargeback rate due to fraud attacks, seasonal demand, or fulfillment issues. Once you cross network thresholds, the response is structured and escalates over time: monitoring programs, fees, required remediation plans, and, in severe cases, account termination by your acquirer.

VAMP and Mastercard thresholds

Under Visa’s VAMP (Visa Acquirer Monitoring Program), the key metric is a combined ratio of TC40 fraud reports and TC15 disputes divided by settled card-not-present transactions.

For merchants in the US, Canada, the EU, and Asia Pacific, the excessive merchant threshold is 2.2% (220bps), dropping to 1.5% (150bps) from April 2026. Merchants in Latin America and the Caribbean are already subject to the 1.5% threshold. Note: VAMP thresholds for Brazil, Chile, and India are yet to be announced separately.

Mastercard uses the Excessive Chargeback Program (ECP). The ECM tier starts at 1.5% with at least 100 chargebacks per month. The HECM tier starts at 3% with 300+ chargebacks

The common advice that "below 1% is safe" is outdated. VAMP combines fraud and disputes into a single ratio, meaning you can breach thresholds even if your chargeback rate alone looks healthy. Acquirers also often enforce merchant-level caps well below Visa's published thresholds.

Once you enter these programs, your options narrow. You need to reduce inflow quickly, decide which disputes are worth fighting, and prevent further escalation before it impacts your ability to process payments.

Penalties and account termination

Once you exceed network thresholds, the escalation is structured and predictable.

It starts with fees and monitoring. You’ll be required to submit remediation plans and show progress in reducing your chargeback rate. If ratios don’t improve, enforcement tightens: higher fees, stricter oversight, and less tolerance from your acquirer.

The final step is account termination. Your acquiring bank can shut down your merchant account, cutting off your ability to process payments. After that, you may be placed on the MATCH list (Member Alert to Control High-Risk Merchants), which makes it significantly harder to get approved by another processor.

This is especially relevant for digital goods and subscription businesses. It’s not uncommon for digital goods and subscriptions to have chargeback rates above the incoming 1.5% threshold, leaving little margin for error.

Who wins chargebacks?

Chargeback outcomes depend heavily on the type of dispute and the quality of your evidence.

That matters more as volumes rise. Mastercard forecasts a 24% increase in chargebacks by 2028, with merchants already attributing 45% of disputes to fraud. A large portion of that fraud is criminal, and those cases are rarely worth contesting, since issuers almost always side with the cardholder.

The cases worth fighting are the ones you can document. Disputes tied to shipping or fulfillment can often be recovered with delivery confirmation, timestamps, and customer communication. Friendly fraud is harder but winnable if you can meet representment requirements like CE3.0.

The ROI comes from choosing the right cases to contest.

Fight, refund, or accept

Not every chargeback should be handled the same way. The goal is to make a cost-based decision:

- Fight when the value is high, and you have strong documentation: delivery confirmation, usage data, or prior transaction history. This is where representment has a clear ROI.

- Refund early when alerts flag a dispute before it becomes a chargeback, and the amount is lower than the cost of fighting. This avoids fees and protects your ratio.

- Accept when the amount is low or the evidence is weak. Fighting these cases adds operational cost without improving outcomes.

If you choose to fight a chargeback, your evidence is reviewed by the issuer, not the customer. Clear, complete documentation submitted quickly is essential.

Chargeback insurance shifts liability to a vendor, but it comes with a trade-off: stricter approval rules and more declined legitimate orders. Many merchants find that detection-focused approaches deliver better overall ROI than insurance-based models, since insurance providers tend to impose stricter approval rules.

Timing matters. Banks typically issue provisional credits quickly while disputes are under review.

Managing chargebacks with Payrails

For merchants running multiple PSPs, chargeback management is fragmented by default. Disputes sit in separate dashboards, evidence is scattered across systems, and building a response means pulling data from payments, risk, and order management tools. That fragmentation slows down response times and lowers win rates, while creating massive bottlenecks for payments and operations teams.

Payrails addresses this by centralizing chargeback workflows across providers, giving teams a single place to manage disputes at scale.

One queue across all PSPs

Payrails centralizes the data that dispute packages and CE3.0 matching require, along with authorization records, risk signals, device fingerprints, and IP addresses from providers like Stripe, Adyen, and more.

Because this data already flows through Payrails, representation evidence can be pulled from a single source rather than fragmented PSP dashboards. Teams can also set response SLAs and use anomaly detection to catch inflow spikes early.

AI-driven dispute packages

Instead of building responses manually, Payrails uses built-in chargeback AI models to generate dispute packages using normalized reason codes and transaction data. Our AI models analyze the documentation submitted by the user (including tracking numbers, service usage logs, and prior transaction history) to construct a highly persuasive, scheme-compliant defense.

By collecting the most compelling pieces of evidence and incorporating them into a structured narrative that addresses the specific chargeback reason code, our chargeback models can maximize the chance of a successful reversal.

These packages can be exported in scheme-specific formats, reducing back-and-forth with PSPs. Outcomes are tracked by issuer and reason code, creating a feedback loop that improves future responses.

What comes after prevention

No prevention strategy eliminates all chargebacks. The ability to intelligently manage chargebacks is what determines how much revenue you recover and how efficiently you operate.

Pricing

Payrails is priced as a platform, not as a share of recovered revenue. We also provide KPI visibility by issuer, country, and PSP, helping you identify patterns that aggregate win rates hide. This makes it easier to connect disputes back to root causes and fix them upstream.

In contrast to the industry standard “share-of-win” pricing, which charges merchants a percentage of recovered revenue, Payrails charges a flat transaction fee, which more accurately reflects the value of improving chargeback workflows and insights – without forcing merchants to pay for chargebacks they likely would have won anyway.

Get chargebacks under control

Most teams try to fix chargebacks at the surface with better fraud tools, clearer policies, and faster support. That helps, but it doesn’t solve the underlying issue: fragmented data and chargeback workflows make chargebacks structurally difficult to manage at scale, while acting as a massive drain on team capacity and resources.

Payrails Chargebacks brings everything into one unified system which uses AI to help you respond to disputes faster, recover more revenue, and understand what’s driving losses.

Book a demo with Payrails today and see the full workflow for yourself.

I am the text that will be copied.